Link to paper

The full paper is available here.

You can also find the paper on PapersWithCode here.

Abstract

- Time series forecasting is an important task in many applications.

- Real-world time series data is often limited and noisy.

- A bidirectional variational auto-encoder (BVAE) is proposed to address the time series forecasting problem.

- The BVAE is equipped with diffusion, denoise, and disentanglement.

- Experiments show that the BVAE outperforms competitive algorithms.

Paper Content

Introduction

- Time series forecasting is important for decision-making

- Traditional RNN-based methods capture temporal dependencies

- LSTMs and GRUs use gate functions to handle long-term dependencies

- CNNs capture complex inner patterns of the time series

- Transformer-based models have shown great performance

- Neural networks have uncertainty issues

- VAR models try to model the distribution of time series

- Interpretable representation learning is another merit

- VAEs have superiority in modeling latent distributions

- Disentangled representation can improve performance and robustness

- Real-world time series are often noisy and short

- D 3 VAE proposed to address time series forecasting problem

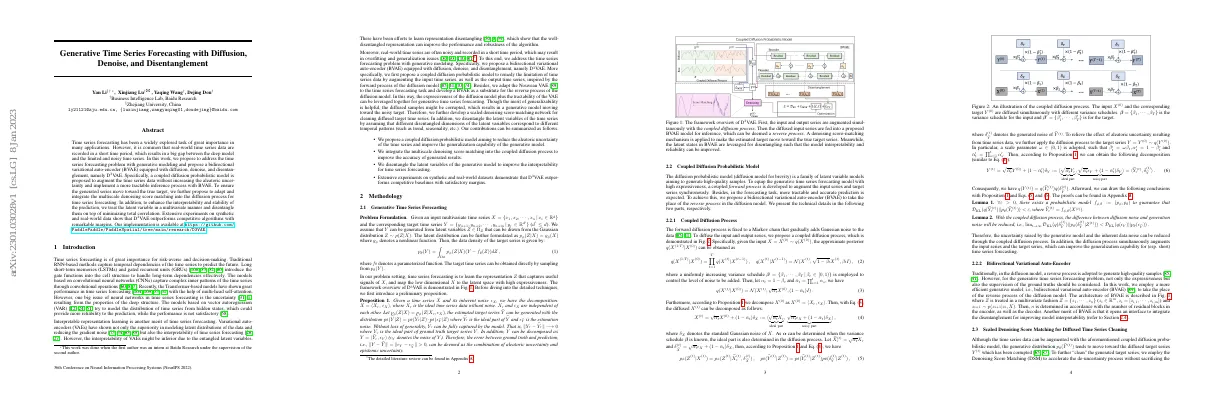

Coupled diffusion probabilistic model

- Diffusion probabilistic model is a family of latent variable models to generate high-quality samples

- Coupled forward process is developed to augment input and target series synchronously

- Bidirectional variational auto-encoder (BVAE) proposed to take place of reverse process in diffusion model

- Markov chain adds Gaussian noise to data

- Coupled diffusion process diffuses input and output series

- Variance schedule and scale parameter used to reduce aleatoric uncertainty

- BVAE opens interface to integrate disentanglement for model interpretability

Scaled denoising score matching for diffused time series cleaning

- Augmenting time series data with coupled diffusion probabilistic model

- Generative distribution moves toward diffused target series

- Employ Denoising Score Matching (DSM) to accelerate de-uncertainty process

- Use monotonically decreasing series of fixed σ values to scale noise of different levels

Disentangling latent variables for interpretation

- Interpretability of time series forecasting model is important

- Disentangling latent variables can enhance reliability of prediction

- Total Correlation (TC) is used to measure dependencies among multiple random variables

- Bidirectional structure of BVAE aggregates rich semantics into latent variables

- Algorithm 1 and 2 used to train and forecast

Training and forecasting

- Proposed coupled diffusion with denoising network to reduce effect of uncertainty

- Minimized TC of latent variables to disentangle them

- Reconstructed loss with trade-off parameters

- Minimized objective to learn generative model

Experiment settings

- Generated two synthetic datasets and six real-world datasets

- Sliced datasets to contain at most 1000 time points

- Compared D3VAE to one GP based method, two auto-regressive methods, and four VAE-based methods

- Used Adam optimizer with initial learning rate of 5e-4

- Batch size of 16 and training set to 20 epochs

- Number of disentanglement factors chosen from {4, 8}

- Evaluation metrics: CRPS and MSE

- Experiments conducted on Linux machine with single NVIDIA P40 GPU

- Experiments repeated five times

Main results

- Two prediction lengths (8 and 16) are evaluated

- Results of longer prediction lengths are in Appendix D

- Noise of outcome series can be estimated to assess uncertainty

- Scale parameter ω can be adjusted to generate distribution space

- Uncertainty estimation can quantify uncertainty effectively

- Disentanglement quality can be assessed by evaluating classification performance

- MIG metric used to evaluate disentanglement

- Diffusion process can effectively augment input or target

Model analysis

- Variance Schedule β and The Number of Diffusion Steps T should be configured properly to reduce the effect of uncertainty.

- Too small a variance schedule or inadequate diffusion steps will lead to a meaningless diffusion process.

- Analysis of the effect of the variance schedule β and the number of diffusion steps T showed that prediction performance can be improved with proper β and T.

Discussion

- Langevin dynamics has been applied to EBMs, computer vision, and natural language processing

- Experiments demonstrate effectiveness of single-step sampling

- Extra empirical study to investigate whether more sampling steps improve performance

- Omitting additive noise in Langevin dynamics and using multi-step denoising for D3VAE

- Different configurations of Langevin dynamics do not bring indispensable benefits for time series forecasting

Conclusion

- Proposed a generative model with bidirectional VAE as the backbone

- Devised a coupled diffusion probabilistic model for time series forecasting

- Developed a scaled denoising network to guarantee prediction accuracy

- Latent variables further disentangled for better model interpretability

- Experiments on synthetic and real-world data validate SOTA performance

- Reviewed related literature of time series forecasting methods

- Complex temporal patterns can be manifested over short- and long-term

- Existing statistical models such as ARIMA and Gaussian process regression

- Temporal attention and causal convolution explored to model temporal dependencies

- Transformer-based models strengthen capability of exploring hidden temporal patterns

- Multivariate nature of TSF another topic many works have been focusing on

- Probabilistic models, matrix/tensor factorization, CNNs, and GNNs

- Generative methods for TSF focus on energy-based models

- VAE-based models to infer underlying distribution of time series data

- Coupled probabilistic diffusion model proposed to augment input and output series

- Multi-scaled score-matching denoising network plugged in for accurate prediction

- Estimate uncertainty for time series forecasting by epistemic uncertainty

- Detect noise in time series data or devise suitable models for noise alleviation

- Neural networks introduced to denoise time series

- Explain deep neural networks to make prediction more interpretable

- Disentangle latent variables to identify independent factors of data

- Bidirectional VAE and take dimensions of each latent variable to be disentangled

- Experiments on synthetic and real-world datasets

- Input representation with embedding method and RNN

- Baselines include GP-copula, DeepAR, TimeGrad, Vanilla VAE, NVAE, f-VAE, and β-TCVAE

- Longer-term time series forecasting and full datasets experiments