Link to paper

The full paper is available here.

You can also find the paper on PapersWithCode here.

Abstract

- Traditional finance uses the Black & Scholes model to price derivatives

- Decentralized Finance (DeFi) and Automated Market Makers (AMMs) are becoming more important

- Liquidity Providers (LPs) are exposed to risks such as Impermanent Loss (IL)

- This paper proposes a method to calculate the greeks of an LP

- Introduces Impermanent Gain, a product that LPs can use to hedge their position and traders can use to bet on a rise in volatility

Paper Content

Introduction

- Overview of computer science ecosystem

- Principal actors in the ecosystem

Decentralized exchanges

- DEXs are peer-to-peer marketplaces for crypto traders.

- DEXs are part of the DeFi suite of financial services.

- DEXs don’t allow for exchanges between fiat and crypto.

- CEXs use an order book to set prices, DEXs use smart contracts and liquidity pools.

- Transactions on DEXs are settled directly on the blockchain.

- DEXs are open-source and developers can create new projects.

Liquidity provider

- Liquidity Providers are investors who fund liquidity pools with crypto assets

- Liquidity Providers are rewarded based on the percentage of the crypto liquidity pool they put, the volume, and the transaction fee offered by the exchange

- Liquidity Provider tokens are given to users who deposit their crypto into a Liquidity Pool and can be redeemed for the underlying assets

- Some platforms require LP tokens to be locked for a period of time to access additional rewards

Constant product amm

- Constant product AMM is a type of AMM

- Reserves of tokens are regulated by a product function

- Uniswap calls the constant L2

- Pool price of token x in terms of token y can be calculated

- Knowing initial data, number of tokens can be calculated at any time

- LP deposits a certain quantity of tokens x and y

- Value of position changes with price

- Fees are paid to protocol and LPs

Hodler

- HODLer is a user that holds tokens without doing anything

- Position value of an HODLer is determined by the change in price of the tokens

- Impermanent Loss (IL) is a problem affecting LPs

- LP and HODLer have starting quantities of tokens

- IL can be expressed in terms of token return

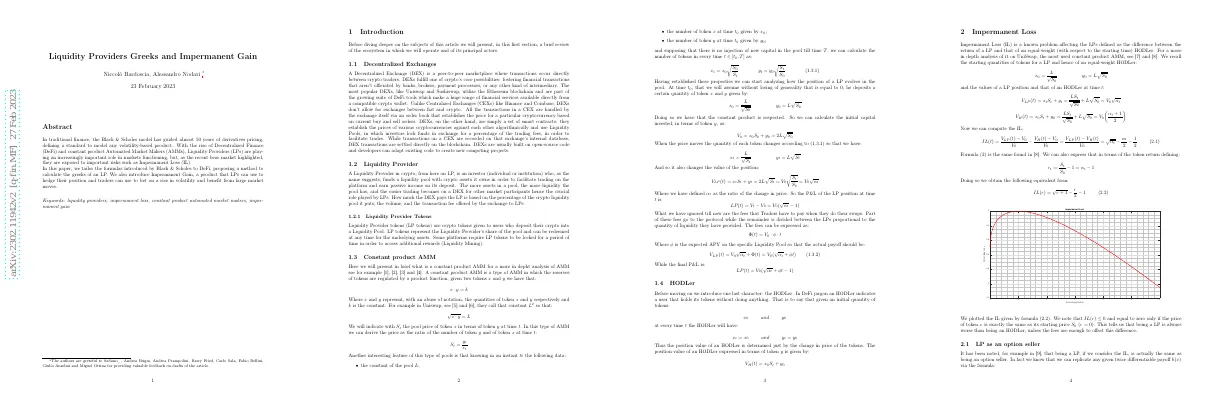

Impermanent loss

- IL(r) is always less than or equal to 0

- IL(r) is equal to 0 only when the price of token x is the same as its starting price

- Being a LP is worse than being an HODLer, unless fees are enough to offset the difference

Lp as an option seller

- Being a LP is the same as being an option seller.

- We can replicate any twice differentiable payoff h(x) with a formula.

- We can replicate the IL by selling an infinite strip of puts and calls of all strikes with maturity T.

Lp pricing and greeks

- LPs can withdraw their liquidity at any time Price of LP position is equal to value of underlying assets plus fees Return of asset x relative to asset y is rt Expected APY is φ Data used for plots: V0 = 10000, S0 = 1000, rf = 3%, σ = 70%, φ = 10%, T = 0.5, τ = 0.25

Unlocked liquidity greeks

- Delta IG (K) is greater than 0

- Gamma IG is greater than 0 and Gamma LP approaches infinity when the underlying price approaches 0

- Gamma 1% is the change of Delta 1% when the underlying price changes by 1%

- Vega is the partial derivative of the price of the position with respect to the volatility

Locked liquidity analysis

- Liquidity Provider locks liquidity until time T

- Fair price of position may differ from value of underlying assets

- Locking liquidity exposes holder to vega and rho risks

- Price process is a Geometric Brownian Motion

- Fair value of LP position can be calculated

Greeks

- Plot of Vega corresponding to 1% change in volatility

- Plot of daily Theta

- Plot of Rho corresponding to 1% change of r f

Impermanent gain

- LP is exposed to many risks

- Product can be structured to hedge all other greeks

- Similarities with European options: maturity T and strike K

- IG payoff can be coded into a smart contract

Pricing

- Replicate IL selling an infinite strip of puts and calls

- Replicate IG buying the same portfolio

- Price IG position by finding cost of replicating portfolio

- Use different approach to price process of token x in terms of token y

- Calculate price of IG strategy at time t as discounted payoff under risk-free measure Q

Impermanent gain as a hedging tool

- Investor provides $10,000 of liquidity on Uniswap ETH/USDC pair

- Investor locks liquidity for 1 year using liquidity mining platform

- ETH price is $1,000

- Investor wants to hedge position using Impermanent Gain